Data Center Investment Is Driving a New Construction Cycle

Billions in Digital Infrastructure Are Fueling What Comes Next

Data centers are one of the fastest-growing segments of non-residential construction, fueled by AI, cloud computing, and digital demand. Billions of dollars are being invested across North America, with thousands of megawatts (MW) under construction. But the real opportunity isn’t just in building the data center. It’s the wave of construction activity that follows the data center.

8,155 MW

Total Energy Supply Going To Data Centers in North America as of H1-2025

35 GW+

Current Energy Capacity Under Construction for Future Data Center Needs

74¢

Of Adjacent Construction for Every $1 Invested in Data Center Construction

$1 Trillion

Expected In Data Center Development in North America by 2030

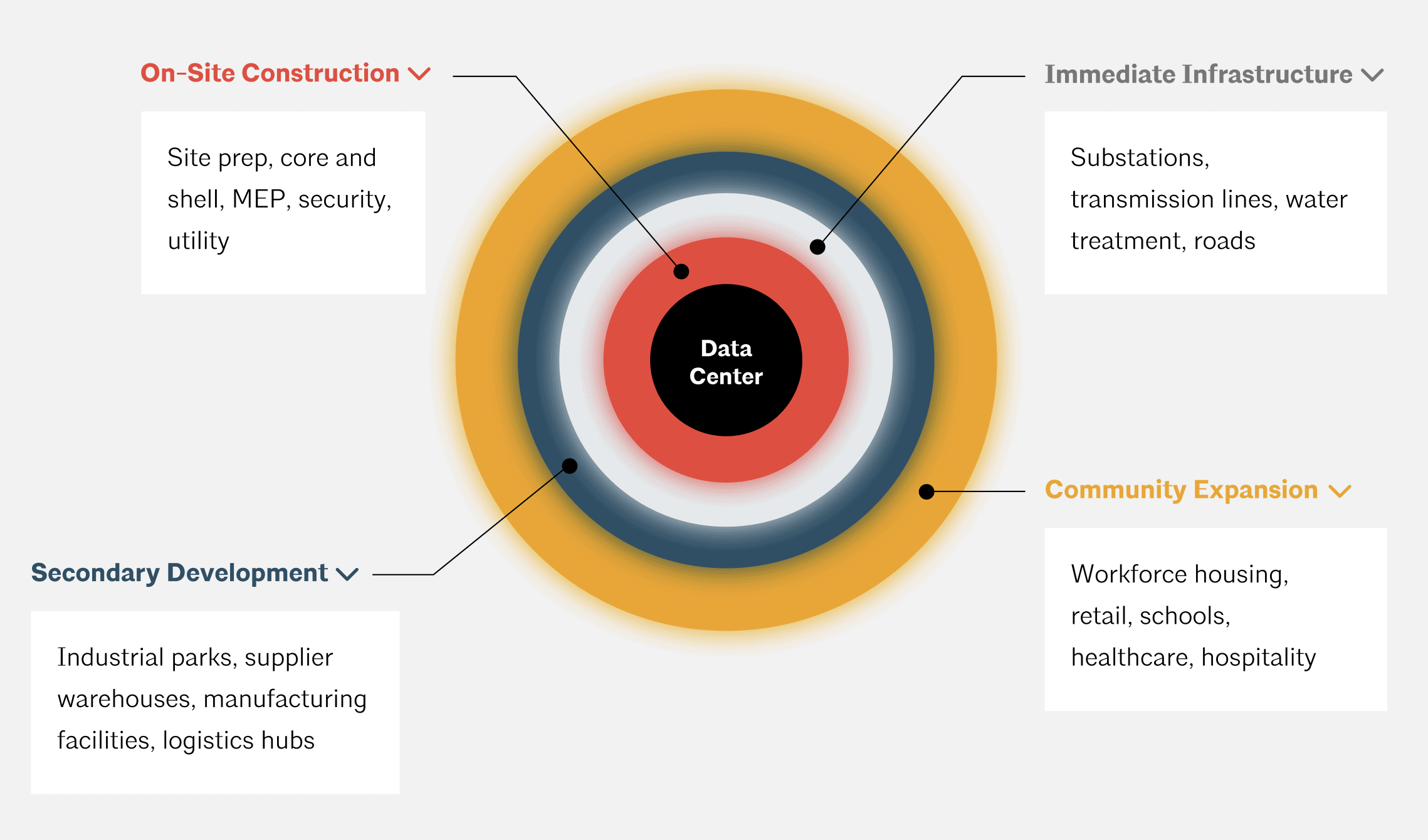

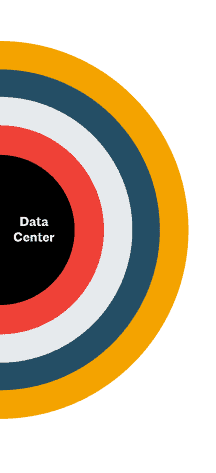

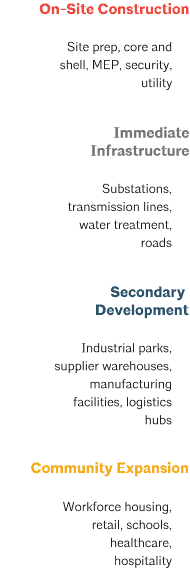

One Project Creates Years of Follow-On Construction

The “Halo Effect” Expands From Site Work to Entire Communities

A data center doesn’t stop at core construction. It triggers a chain reaction, with power infrastructure utilities and site development coming first. Followed by industrial, logistics, and supplier facilities. Over time, population growth drives housing, retail, healthcare, and schools. What began as a single project is now a multi-year construction pipeline across sectors.

Workforce Growth Fuels Community Expansion

New jobs drive population growth. That demand quickly translates into housing, retail, infrastructure, and essential services. For builders, this is where the next wave of accessible, high-volume projects begins.

They accelerate:

Residential Growth

Retail Development

Warehousing

Infrastructure

Office Space

Workforce Housing

Schools

Hospitality

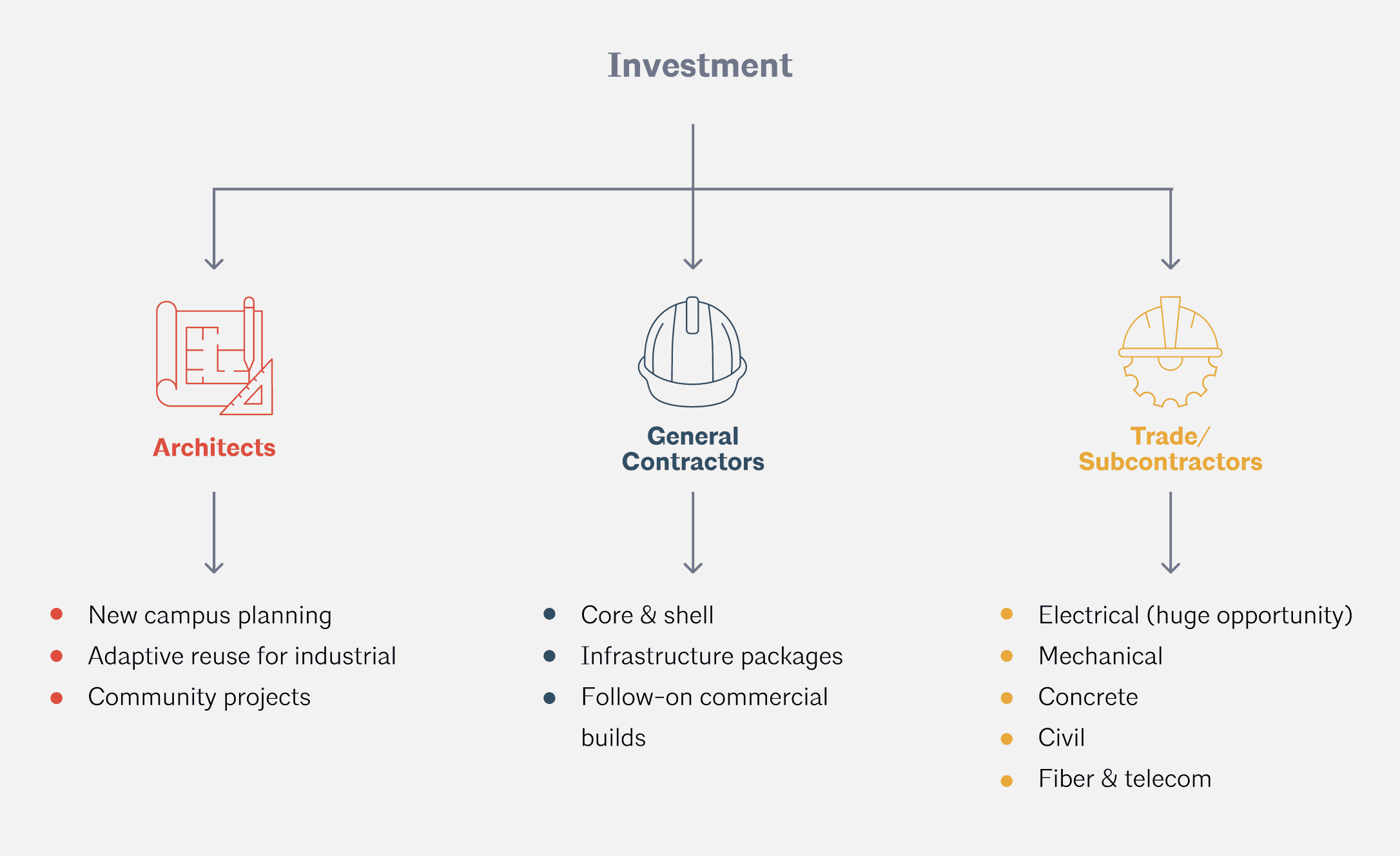

Every Role in Construction Benefits from Data Center Growth

From Architects to Contractors, Work Expands Beyond the Core Build

Hyperscale facilities may be specialized, but the surrounding work is not. Architects design new communities. General contractors build commercial and infrastructure projects. Across every phase, trade contractors (especially electrical, mechanical, and civil) experience sustained demand. As investment enters a market, it creates a ripple effect of accessible projects for the broader construction industry.

Data Center Activity Signals Where Construction is Headed

Jobs, Infrastructure, and Permits Point to Future Demand

A single 1 GW data center can generate tens of thousands of construction jobs and long-term economic activity. That growth shows up quickly in permit activity, utility expansion, and mixed-use development.

What construction of a 1 GW data center creates:

45,367

Temporary Jobs (Many in AEC Industry)

$405.8M

In Recurring State and Local Tax Revenue

5,322

High-Paying Permanent Positions Support the Facility Once Operational

Track These Signals To Anticipate What’s Next

Identify where demand is forming and position your firm before projects hit the mainstream pipeline.

Builders who track hyperscale investments can anticipate:

Zoning Changes

Utility Expansions

Residential Permits

Mixed-Use Planning

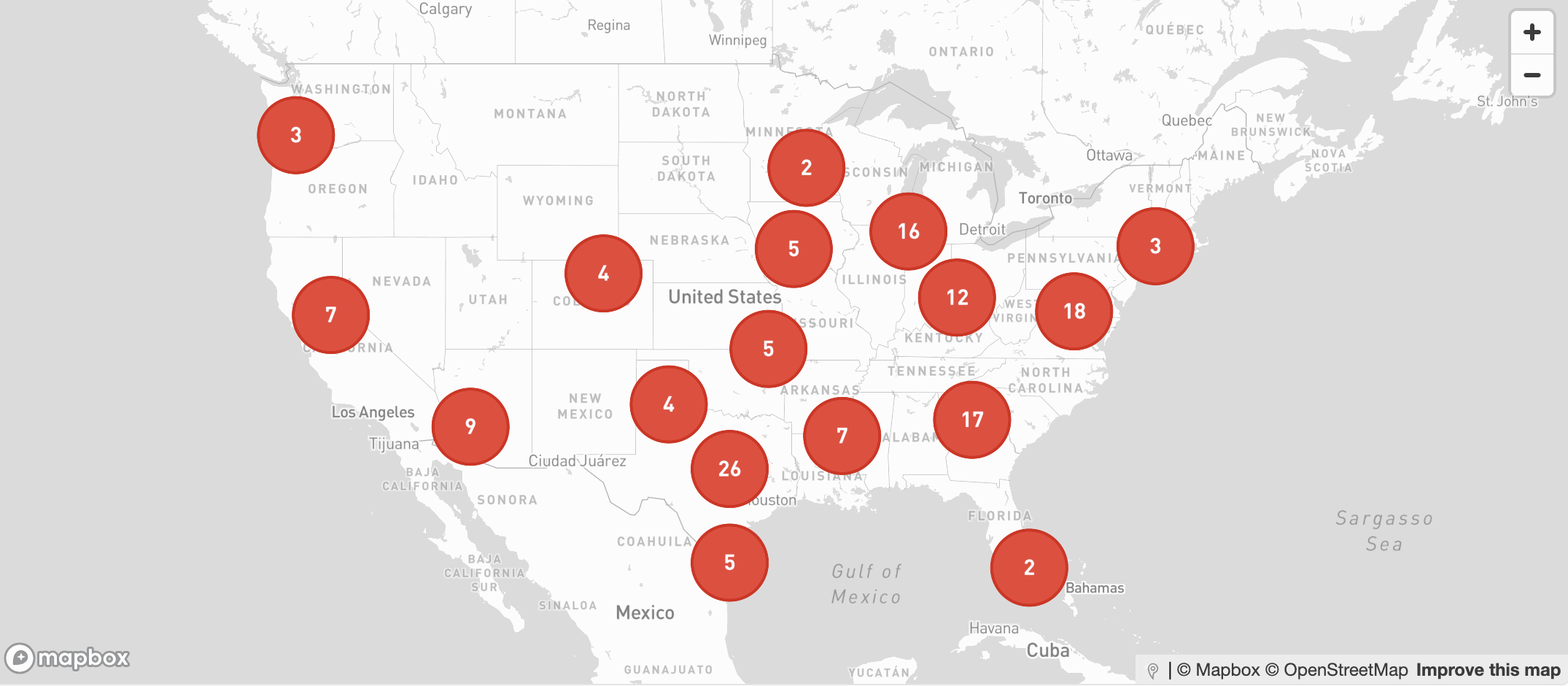

Turn Data Center Growth into Your Next Project Pipeline

See where hyperscale investments are happening and uncover the infrastructure, housing, and commercial work that follows.